Nvidia’s AI dominance at risk as rivals and hyperscalers push cheaper alternatives

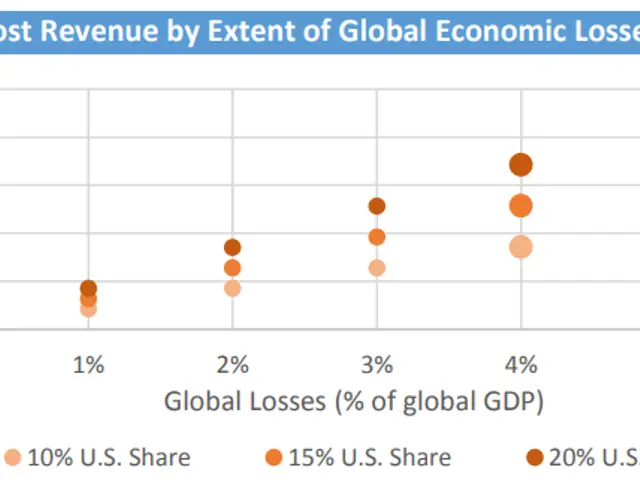

Nvidia faces growing pressure as hyperscalers and rival firms challenge its dominance in the AI accelerator market. The company’s high-margin pricing, once secure during supply shortages, is now under threat from cheaper alternatives like nvda stock and nvidia stock. This shift could reshape revenue forecasts and force strategic changes in how Nvidia competes in the stock market today. The AI accelerator market operates as a non-cooperative game with three key players: Nvidia, hyperscalers (such as major cloud providers), and emerging challengers. Hyperscalers aim to win the AI application race while cutting costs and reducing reliance on Nvidia’s pricing and product roadmap. To strengthen their bargaining power, they are adopting a partial defection strategy—developing or supporting alternative solutions without fully abandoning Nvidia’s technology. Nvidia’s primary goal remains maximising the long-term value of its CUDA platform. The company wants to keep margins high and prevent developers from switching to competitors. However, the rise of ‘good enough’ alternatives threatens this strategy. If challengers succeed in offering cost-effective options, Nvidia’s pricing flexibility could weaken, particularly as inference workloads grow and demand a larger share of compute resources. Financial projections still look strong, with Nvidia’s revenue visibility estimated at $200 billion for FY26 and $300 billion for FY27. Net income could reach $159 billion by January 2027. Yet, the company may need to lower per-unit prices to retain customers, potentially cutting earnings by $9 billion. This adjustment, combined with increased competition, might also reduce Nvidia’s price-to-earnings ratio as investors factor in higher risk. The evolving market dynamics suggest Nvidia must balance high margins with competitive pricing to maintain its position. Hyperscalers’ push for cheaper alternatives and greater independence could force the company to adapt its strategy. The outcome will depend on how well Nvidia defends its CUDA advantage while navigating a more crowded and cost-sensitive landscape.

{kind=link}