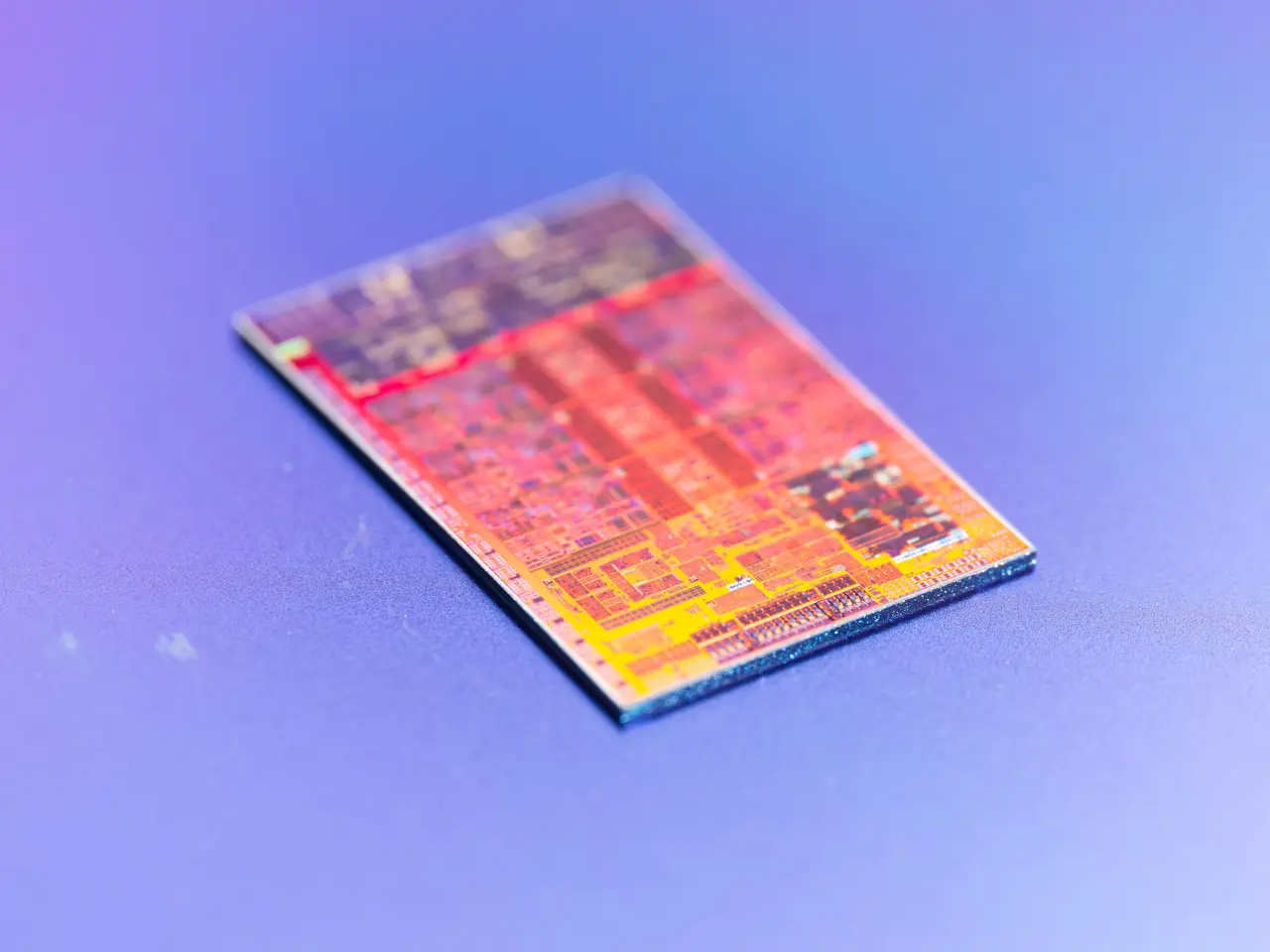

Micron's bold $25B chip bet clashes with delays and fierce competition

Micron faces a mix of challenges and strategic moves as it navigates a shifting semiconductor market. Despite reporting record earnings guidance for Q2, the company's stock price has fallen, with analysts now targeting a 28.1% downside to $254 per share. Meanwhile, delays in major projects and rising competition are reshaping its near-term outlook. Micron has raised its fiscal 2026 capital expenditure by over $25 billion to speed up domestic chip production. This push comes as it ramps up output of advanced 1-gamma DRAM and G9 NAND, aiming to stay ahead in memory technology. The company has also begun securing five-year supply agreements with key customers, offering long-term stability in an otherwise volatile market.

The construction of Micron's $100 billion New York megafab has hit a setback, with the first phase now delayed until Q3 2030. Labour shortages and complex building requirements have slowed progress, pushing back initial production timelines. This comes as competitors Samsung and SK hynix prepare to enter the HBM4 market, raising concerns about a potential price war that could squeeze Micron's profit margins.

Beyond manufacturing hurdles, broader industry trends add pressure. Hyperscalers like Amazon and Google are absorbing long-term energy costs, which may reduce their available capital for high-bandwidth memory (HBM) investments. Additionally, AI adoption remains uneven—only 34% of organisations have fully deployed AI agents, and up to 95% of enterprise AI pilots fail to meet expectations, potentially dampening demand for advanced memory solutions. Micron's stock now trades at a P/E GAAP ratio of 16.72, lower than rivals Samsung and Broadcom, with a free cash flow yield of 2.4%. The company's aggressive expansion and long-term contracts aim to offset risks from delayed projects and intensifying competition. However, its near-term performance will depend on how quickly it can stabilise production and adapt to shifting market demands.

{kind=link}