EU's Russian energy cutback hits snags as LNG imports rise

The EU's push to cut ties with Russian energy has faced mixed results since the invasion of Ukraine. While pipeline gas imports have dropped sharply, the bloc's reliance on Russian liquefied natural gas (LNG) has grown. New data reveals a complex shift in Europe's energy strategy, with some countries still dependent on Russian supplies despite political pressure to phase them out entirely.

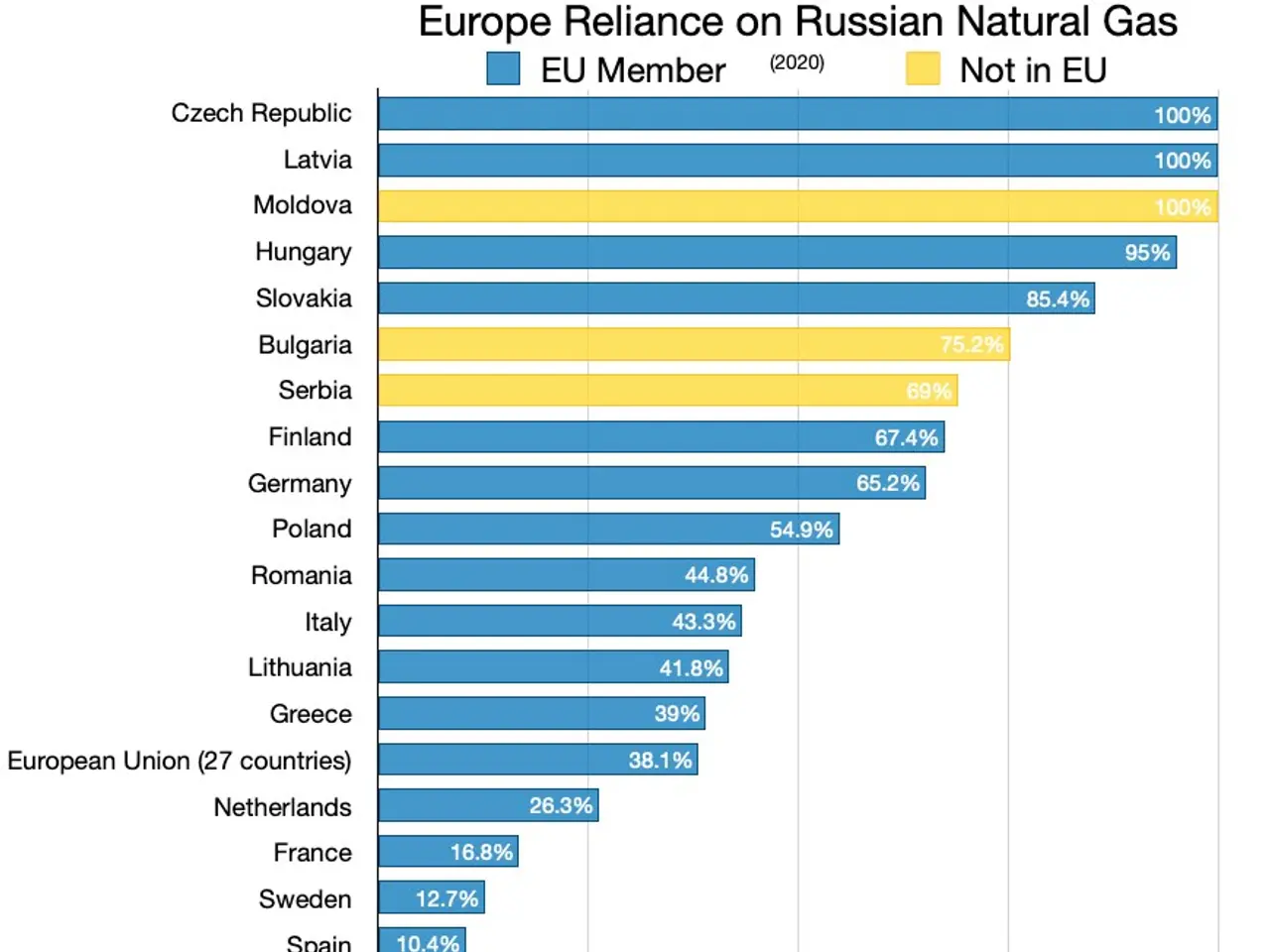

Before the war in Ukraine, Russian pipeline gas made up 40% of the EU's gas imports. By 2024, that share had fallen to around 11%. Yet the overall picture is more complicated. The EU's total imports of Russian gas actually rose by 18% in 2024, driven largely by increased LNG purchases—some of which still originate from Russia, either directly or indirectly.

The decline in pipeline gas has been steep in certain countries. Italy, once a major buyer, cut its imports from 40 billion cubic metres (bcm) in 2021 to under 5 bcm by 2023. The Czech Republic halted pipeline imports entirely, while France reduced its intake to minimal levels. However, the role of Russian LNG in these reductions remains unclear, as detailed figures on its contribution are scarce. Since February 2022, the EU has banned most seaborne Russian crude oil imports, but pipeline deliveries via the Druzhba Pipeline were exempted for landlocked nations like Hungary. This exemption has kept some Russian oil flowing into Europe, despite criticism. Hungary's continued purchases reflect broader structural dependencies, challenging the narrative that it is the only EU country still buying Russian energy. The EU's long-term plan to phase out Russian energy hinges on three key assumptions: finding alternative suppliers, adapting to market changes, and enforcing reliable regulations. Yet the recent rise in LNG imports—including those with Russian links—shows how difficult a full break from Russian energy has become. Countries like Italy, France, and the Czech Republic, despite cutting pipeline gas, have still increased their LNG intake, some of which may be Russian in origin.

The EU's energy transition remains uneven, with progress in reducing pipeline gas offset by a rise in LNG imports. While political commitments to phase out Russian energy are strong, market realities and existing contracts continue to shape Europe's supply. The challenge now lies in balancing strategic goals with the practical need for stable energy sources.

{kind=link}